As part of the revision of the Swiss insurance supervisory framework, FINMA has restructured the regulatory requirements governing insurers’ investment activities and tied assets (gebundenes Vermögen). These changes form part of the broader revision of the Insurance Supervision Act (VAG) and its implementing ordinances.

The revised framework aims to strengthen policyholder protection while enhancing the competitiveness and flexibility of the Swiss insurance sector. A key element of this reform is the transition from detailed prescriptive requirements towards a more principle-based regulatory approach, centred on the prudent person principle.

From 1 January 2024 onwards, FINMA Circular 2016/5 will be replaced by provisions embedded within the revised AVO and the new FINMA-AVO.

Regulatory Evolution

Historically, requirements for tied assets were primarily governed by FINMA Circular 2016/5, which defined detailed quantitative limits and eligibility criteria for assets covering the target amount (Sollbetrag).

Under the revised framework effective from 1 January 2024, the circular is formally repealed and its existing requirements are redistributed across the AVO and FINMA-AVO. The regulatory structure is thereby reorganised along a more hierarchical and principle-based approach.

While many quantitative limits remain, their formulation is less granular, with greater emphasis placed on insurers’ internal governance and risk management.

Key Changes under AVO and FINMA-AVO

The transition introduces several overarching changes. Most notably, the framework shifts from a rule-based to a more principle-based approach, with stronger reliance on the prudent person principle. Tied asset requirements are now consolidated within formal ordinances rather than circular-level guidance, creating a more structured legal hierarchy. In selected areas, the regime becomes less prescriptive, allowing insurers greater flexibility in asset allocation and asset-liability management (ALM) practices. At the same time, the framework continues to rely on quantitative limits, although with less detailed implementation guidance than under the previous circular.

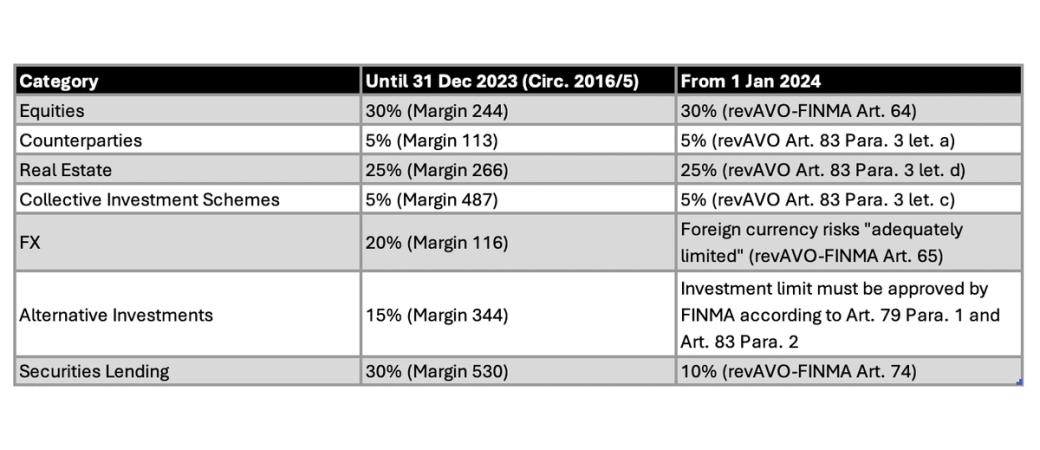

These are the key changes from 31 December 2023 to 1 January 2024, when Circular 2016/5 is replaced by revAVO / revAVO-FINMA:

Relevance for Tied Asset Coverage Calculations

For the calculation of the coverage of the target amount (Sollbetrag) by tied assets, we observe the following key implications:

1) Core quantitative constraints remain largely unchanged

The main limitations previously defined under Circular 2016/5 continue to apply under AVO and FINMA-AVO. These include asset class limits, counterparty concentration limits, and maximum exposure to individual fund holdings.

2) Exemptions remain consistent

Existing exemptions from counterparty concentration limits remain in place, including exposures to the Swiss Confederation, cantons and Pfandbriefe institutions. In addition, the general exemption for funds classified as non-high risk continues to apply.

3) Foreign exchange exposure requirements are less prescriptive

The previous explicit limit allowing up to 20% foreign currency exposure to cover the target amount is no longer explicitly defined. Instead, foreign exchange risks must now be “adequately limited”, implying a more judgement-based supervisory assessment.

4) Revised exemption rules for fund concentration limits

The treatment of collective investment schemes exceeding 5% of the target amount has been updated. The revised framework replaces detailed asset eligibility lists with a principle-based definition of “non-high risk” investments. Exemptions now rely on contractual assurances and adherence to tied asset principles rather than predefined asset categories.

5) Continued relevance of look-through requirements

Investments into collective investment schemes remain subject to the requirement that underlying assets qualify as eligible assets under Article 79 AVO. In practice, this implies that look-through reporting remains necessary, including for fund-of-funds structures.

High-Level Assessment

At a high level, the revised framework preserves the core economic and risk management principles governing tied assets.

However, compared to Circular 2016/5, the new regime introduces:

- A stronger emphasis on the prudent person principle

- Less granular and less prescriptive requirements

- Increased reliance on insurer-specific judgement and internal processes

While the quantitative backbone of the regime remains largely intact, the practical implementation is expected to require enhanced documentation, more robust internal risk assessments, and continued use of look-through analyses for collective investments.

Implications for Our Services

The regulatory changes are not expected to fundamentally alter tied asset coverage calculations. However, they introduce adjustments in methodology, interpretation and documentation, particularly in the following areas:

- Assessment of foreign exchange exposure under principle-based constraints

- Evaluation of fund eligibility under revised exemption rules

- Continued monitoring of concentration and asset class limits

- Increased importance of look-through reporting and transparency

Through our managed service, we support clients in data acquisition, validation, look-through analysis, and advisory on the implementation of the revised framework.

References

- FINMA – Investment activities from 1 January 2024 onwards: tied assets and investment guidelines

- Revision of the Swiss Insurance Supervision Act (VAG), AVO and FINMA-AVO

- FINMA Circular 2016/5 (repealed as of 1 January 2024)